Gold Price Supported Above Producer Break-Even Levels?

Talking Points:

-Historical price action says producer break-even levels serve as an informal gold price floor.

-Although QE3 is set to end by the end of the year, will central banks globally fill the Fed’s shoes?

-Opportunities in 2014 to establish longer term positions?

Gold is a commodity that is the king of trends, be them bullish or bearish, and it may be useful to take a longer term approach to price action. For one, there are a myriad of factors that impact the price of gold and looking at each of them individually may not be the best way to achieve a sound hypothesis. To be frank, the more uncertain variables we include (inputs) the less likely we are to be correct in our outcome. General themes that have held true over history may prove valuable in any approach.

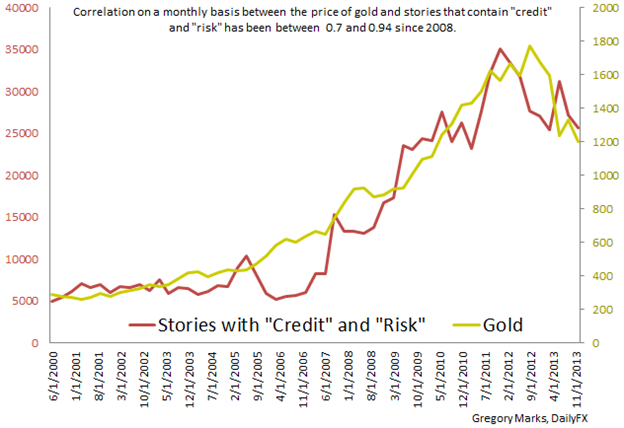

Gold Price and Key Terms Correlation Chart

For one, a major historical theme is when we approach producer break-even levels on production, we find support. Former Fed Chairman Ben Bernanke said in 2013 that “no one really understands gold prices” and that it is an “unusual asset,” but in fact it may be the most usual and logical asset of all (on a medium to long term basis). The degree to which we deviate from said supportto the downside has been quite limited throughout history as thebid generally comes forth. In addition, in those rare instances where gold has fallen below established or estimated breakeven levels, it has not stayed there for long.

More established miners such as Barrick are assuming a $1,100 gold price in 2014 vs. a $1,500 assumption in 2012. Assuming such a high spot price in 2012 just shows the extent to which miners were overextended in the run-up and that fact is representative of their prior unwillingness to challenge the idea of a major correction. The $1,100 figure is much more conservative and in line with estimates of producer breakeven levels.

In regards to monetary policy, gold bulls at these general levels make the argument that with the Fed removing QE3 by the fourth quarter of 2014, bulls don’t have a case. Although at the surface the argument is sound, we must not discount the fact that a number of central banks may have to take the place of the Fed in the coming years. Speculation is making the rounds that the Bank of Japan may have to ease further by this summer on declining prospects post-sales tax hike and just today Draghi said that the council is discussing what an ‘EU QE’ would look like if it did have to be implemented.

Although Mr. Draghi has said he expects inflation to pick up in April, it is important to put CPI figures in the context of a 5yr seasonality average. If historical trends tell us anything, the second quarter and early/mid third quarter may not prove as smoothly as some policy makers have stated.

Although we can put forth fundamental factors for medium to long term trends, observing near term price action is always key: DailyFX Gold Price Articles.

Gregory Marks, DailyFX Research Team

Keep up to date on event risk with the DailyFX Calendar.

How does a Currency War affect your FX trading?

original source

Indonesia

Indonesia