INR – Rupee Survives Emerging Market Selloff Amid Confidence in RBI

RBI’s Raghuram Rajan has stuck true to his rhetoric on how he would handle RBI policy in 2014.

Talking Points:

-USD/INR remains well supported despite EM selloffs

-Confidence in the RBI remains strong under Raghuram Rajan

-Market participants look to CPI data, relatively stable growth

Since our January special report on the Reserve Bank of India and the Indian economy, fundamentals have largely remained the same despite further headwinds in emerging markets. Since those reports, we have seen a number of key data figures released including the RBI’s January Repurchase Rate, Industrial Production, 4Q GDP figures and Wholesale Prices. In addition, optimism on the political front ahead of the April 7th-May 12th election cycle has boosted investor confidence on the economy.

|

DATE |

2014 DATA |

ACTUAL |

SURVEY |

|

01/10 |

Industrial Production YoY (NOV) |

-2.1% |

0.8% |

|

01/13 |

CPI YoY (DEC) |

9.87% |

10.0% |

|

01/28 |

RBI Repurchase Rate |

8.00% |

7.75% |

|

02/12 |

Industrial Production YoY (DEC) |

-0.6% |

-1.2% |

|

02/14 |

Wholesale Prices YoY (JAN) |

5.05% |

5.60% |

|

02/28 |

GDP YoY (4Q) |

4.7% |

4.7% |

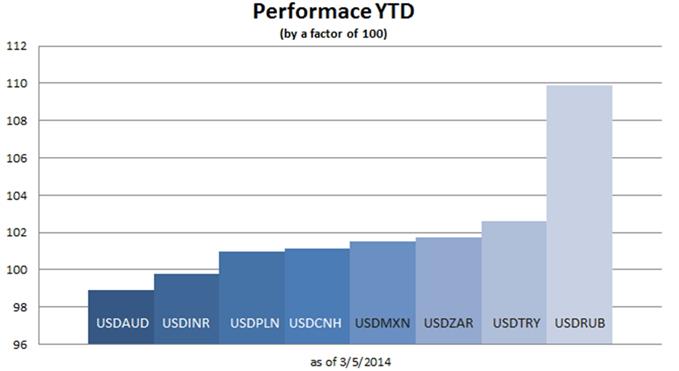

At the January meeting, Raghuram Rajan stuck true to his rhetoric on how he would handle RBI policy moving forward. The central bank hiked rates by 25bps (basis points) to 8.00%, thus marking the third increase since the summer of 2013. In an environment where major emerging market central banks are raising rates drastically and unexpectedly to protect their currencies against selloffs, the Rupee continues to remain well supported amid confidence that Dr. Rajan can truly lead the RBI. Looking at the chart below we can see that among major EM currencies, the Indian Rupee has held up the best against the US dollar (USD). For reference and to represent the relative strength of INR, we have included the Australian Dollar (far left).

USD/INR - Indian Rupee Performance Table

If major EM turmoil has been unable to hit the Rupee so far this year, it may be likely that excluding unprecedented market disturbances, market participants will be trading the Rupee in the context of incoming CPI data over the next few months. Dr. Rajan has made it clear that he is willing to have slower near term growth in exchange for healthier prices moving forward and this has been largely welcomed across the board. This gives the RBI leeway when incoming economic data disappoints so long that we do not see a severe slowdown. At this current juncture, it appears as though gradual rate increases are having their intended impacts of lowering price levels. Fundamental prospects may continue to remain supportive of the Rupee if such trends continue. It is also important we note that the nine series election cycle stretching from early April to mid-May is likely to support Indian prospects so long that the opposition party (under leader Narendra Modi) remains ahead in the polls. Foreign investors have shown a liking to the party as it seeks to shake up corruption on the political front and this has helped further Rupee strength in recent weeks.

|

Date |

Upcoming Event Risk |

|

03/12 |

Industrial Production YoY |

|

03/14 |

Wholesale Prices YoY |

|

04/01 |

RBI Repurchase Rate |

|

4/07-05/12 |

National Elections |

Gregory Marks, DailyFX Research Team

To contact Gregory Marks, e-mail [email protected]

original source

Indonesia

Indonesia