USD/INR: Indian Rupee Selloff to Resume as Optimism Fades?

Talking Points:

-April/May election results pose risks to INR, Rupee optimism.

-Seasonal inflation tends to rise into year end, agricultural prices YTD unusually high already.

-Rupee sell-off could resume into 2Q/3Q, especially in the context of USD recovery.

Last week we highlighted risks to the Indian Rupee that are likely to start as the second quarter gets underway. For one, expectations on the fundamental front have not felt this positive for some time. Partly attributed to brightening prospects on the back of higher U.S. growth, optimism in the Reserve Bank of India and the current election cycle have helped further fuel the recent Rupee strength. This has all occurred in the context of a weaker Dollar with the Dow Jones FXCM USDollar Index down 2.6% from YTD highs at the time of this report.

The underlying issue with current expectations is that actual results cannot be determined for some time and sentiment is overly optimistic on multiple fronts. At this current juncture, the market has been pricing the Rupee as if elections will go in the opposition party’s favor, growth will not falter and the RBI will be successful in capping inflation. Post-election euphoria has faded before and is likely to fade again, especially in the context of price levels that tend to rise into year end.

USD/INR Daily Chart

At the end of January we made the fundamental case that the Indian Rupee could see strength as confidence in the Reserve Bank of India picked up in 2014, but that confidence currently looks to be stretched. Although the central bank remains committed to targeting price levels, this is a longer term theme and the central bank is likely to struggle in the second and third quarter when CPI seasonally picks up. On April 15th we received Wholesale Price data for March that came in at 5.7% vs. 5.3% expected YoY. CPI data also came in higher than expected at 8.31% vs. 8.25% surveyed.

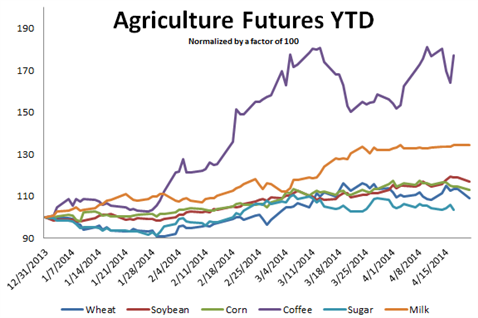

The CPI basket in India consists of a larger than usual weighting toward food prices and the fact that agricultural prices are already unusually high year-to-date is disconcerting and a risk to optimism that market participants hold on the monetary policy front. Poor weather in the first quarter has impacted yields and fears of supply disruptions in the grain market on Ukraine/Russia tension has added to YTD price action. Higher CPI figures out of India on these developments in agricultural prices may help support USD/INR into the second and third quarters.

Gregory Marks, DailyFX Research Team, FXCM

Keep up to date on event risk with the DailyFX Calendar.

How does a Currency War affect your FX trading?

original source

Indonesia

Indonesia