Euro?s Potential Capped as Regional Growth Grinds to a Halt

Fundamental Forecast for Euro: Neutral

- European growth data was surprisingly bad over the course of the week…

- …but market participants haven’t decided to send the Euro lower just yet.

- Have a bullish (or bearish) bias on the Euro, but don’t know which pair to use? Use a Euro currency basket.

The Euro’s rarely been a top or worst performer over the last several weeks, treading water as several other major currencies’ problems have cropped up in the interim. This week was no different: EURGBP, the top performing EUR-cross, finished up by +0.41%; and EURCAD, the worst performing EUR-cross, finished down by -0.77%. EURUSD was little changed, up by +0.07% to $1.3401.

Certain factors influencing the Euro haven’t proved to be negative. Liquidity conditions, for example, remain ample. Euro-Zone excess liquidity rose to €134.9B on the week, and the interbank lending rate (EONIA) was pinned at 0.014%. Fears of a sovereign debt crisis are nothing but a memory at this point; sovereign yields across the continent are at or near all-time lows, regardless of duration.

The lack of change in Euro exchange rates can be partially attributed to the limited movement in the corresponding futures market: non-commercials/speculators net-short positions were reported at 126.0K contracts per the CFTC’s report issue on Friday, a hair lower than the 128.7K net-short contracts held at the end of the prior reporting period. This was the first decline in net-short positions since the week ended July 8.

Unfortunately, the Euro’s midweek hiccup, resulting from the surprisingly poor French, German, and broader Euro-Zone Q2 GDP data, isn’t reflected in the CFTC’s positioning update (the reporting window closed on Tuesday; the GDP figures came out on Thursday).

What we can tell though is that European data momentum slumped once again, which offers little reason for speculators holding net-short Euro positions to ease off their bias. The Citi Economic Surprise Index slipped back to -35.2 at the end of this past week, barely above the yearly low set on July 21 at -43.3.

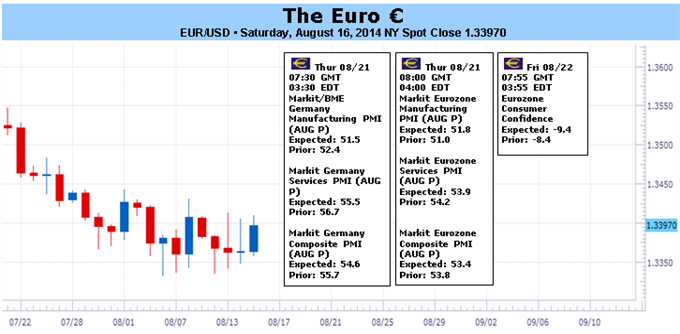

The upcoming preliminary August German and Euro-Zone PMI surveys aren’t forecast to see the weak growth trend get any better. The reports, released on Thursday, across each the Manufacturing, Services, and Composite indexes for Germany and the Euro-Zone are expected to decline from their July readings. You can view all six forecasts in the DailyFX Euro Economic Calendar.

When we take a step back, the bad has outweighed the good, and we haven’t even discussed the Russian sanctions. Truth be told, there is probably some feedback into the weak Q2 GDP figures as tensions from the Russia-Ukraine conflict evolved, and there will be going forward.

Considering the Q2 GDP figures were so flat and inflation at +0.4%y/y was the tenth consecutive month below +1.0%y/y, the ECB might overlook the pristine liquidity conditions it created. As the Russian-Ukrainian crisis wanes on business relationships and the sudden stop of trade between two significant partners (EU and Russia), there is bound to be economic fallout. Put simply, the ECB may be forced to compensate a bit more for exogenous risks, and speculation of additional easing action on these premises may be enough to prevent a true comeback by the Euro. –CV

To receive reports from this analyst, sign up for Christopher’s distribution list.

original source

Indonesia

Indonesia