Euro Rebounds Prove Shallow as Euro-Zone Sits on Cusp of Recession

Fundamental Forecast for Pound:Neutral

- It appeared that EURUSD would be afforded an opportunity to rally after the FOMC’s commentary on Wednesday.

- Mounting concerns over global growth hurt the Euro, triggered classic ‘risk off’ mode at the end of the week.

- Have a bullish (or bearish) bias on the Euro, but don’t know which pair to use? Use a Euro currency basket.

The Euro was afforded a modest rebound this past week as the US Dollar’s historic 12-week bull rally came to an end. Still, with gains capped at no more than +0.89% (against the US Dollar), the Euro’s reversal can be considered shallow at best. With risk assets retreating globally, EURJPY posted the biggest loss of any EUR-cross – it’s usually an ominous sign when the Yen is the top performer.

Although the Euro-Zone hasn’t been an engine of global growth the past few years, it is still the largest aggregate economic zone in the world. Nevertheless, much of the recent weakness in risk assets can be attributed to the region’s quickly diminishing growth prospects. Equity markets, notably the German DAX, have plunged to fresh yearly lows amid a fresh wave of downtrodden growth data.

Two pieces of German data this past week in particular have stoked concern about economic downturn anew in the Euro-Zone’s largest economy. August German Factory Orders plunged by -5.7% m/m, more than double the expected decline of -2.5% m/m. Likewise, August German Industrial Production contracted by -4.0% m/m, nearly triple the forecast -1.5% m/m decline. The economic decline is seen region-wide, with the Citi Economic Surprise Index hitting a fresh yearly low at -57.1 on October 10.

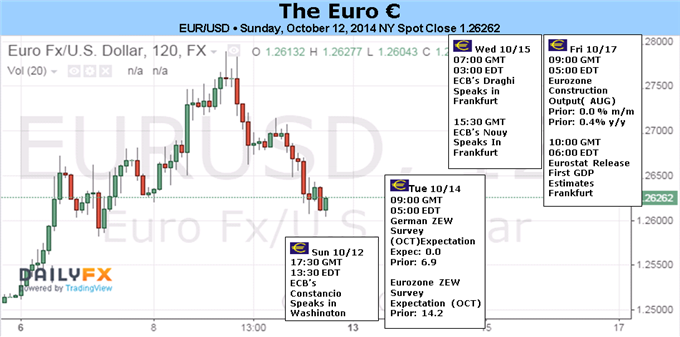

The week ahead should bring forward additional signs of dour developments out of the region. October German ZEW Survey data released on Tuesday threatens to show a further deterioration at a time when concerns about German Q3 growth have started to crop up. The Current Assessment portion of the survey is expected to come in at 15.0 from 25.4, well-below the yearly high set in June at 67.7. The Economic Sentiment portion of the survey is due at 0.0 from 6.9, off the yearly high set in January at 61.7.

Also due on Tuesday is the August Euro-Zone Industrial Production report which should be weighed heavily by the weak German figures released in the week prior, which severely limited the Euro’s rebound. The final September Euro-Zone Consumer Price Index release on Thursday should confirm the disinflationary +0.3% y/y prior release; yet with the Euro’s >-6% depreciation since its May high of $1.3993 against the US Dollar, a bottoming in inflation figures may develop in the coming months.

Even as the trade-weighted Euro basked has managed a meager bounce from its yearly lows (EURUSD itself closed the week at $1.2626, up from the $1.2501 low set on October 3), futures traders’ sentiment has changed very little. Net non-commercial/speculative positioning stood at 146.2K net-short contracts, just off the slightly more extreme positioning of 161.4K net-short contracts for the week ended September 2.

With FXCM’s SSI showing that the retail crowd flipped from net-long to net-short momentarily mid-week, it’s evident that the lack of continuation downward has shaken out some of the less patient short hands. This could be a sentiment turning point: if the crowd stays net-short on a EURUSD move through $1.2700, the futures market positioning may provide enough kindling to provoke a decent short covering rally. That day may be farther away now, as the recent economic downswing has traders bracing for the third leg of the Euro-Zone recession. –CV

To receive reports from this analyst, sign up for Christopher’s distribution list.

original source

Indonesia

Indonesia